The FCA’s Conduct of Business Sourcebook (COBS) is a set of regulations that governs how financial firms communicate and promote their services to ensure fairness and transparency in the financial markets. Disclaimers and disclosures are essential elements of this framework, helping prevent fines, lawsuits, and suspensions. Over 90% of our Financial Services clients express concern about compliance, especially given that the FCA blocked over 8,500 ads in 2022.

Penalties for any breaches in financial marketing compliance are harsh. Notably, WealthPress was ordered to refund over a million USD for misleading claims in 2023.

What is the Key Objective of the COBS?

The FCA’s COBs Sourcebook is a critical component of the FCA Handbook, establishing rules and principles that financial firms must follow when communicating with customers. Its number one objective is customer protection and seeks to ensure that by receiving honest and understandable communications, they will be in a position to make informed financial decisions.

Firms are held accountable for their communications, which must be consistent and truthful.

Understanding the FCA

The Financial Conduct Authority (FCA) is the UK’s independent financial regulator. Its role is to protect consumers and ensure firms comply with the law. The FCA oversees a wide range of activities, including anti-money laundering and consumer credit plans. FCA compliance means adhering to all regulations. Without the FCA, firms would face direct government scrutiny, leading to severe consequences, including jail time for serious violations.

Staying Compliant with Changing Rules

The FCA and His Majesty’s Treasury (HMT) review disclaimer and disclosure policies, which may lead to new requirements, such as character limits and formatting changes. Similarly, the SEC’s recent “New Marketing Rule” includes enhanced disclosure requirements for investment advisors.

IntelligenceBank helps you maintain compliance with FCA regulations by using AI to identify risks in marketing assets and automate compliance feedback, reducing the back-and-forth between marketing and legal teams.

Common Types of Disclaimers

With strict FCA regulations governing the marketing of financial products, companies have to navigate a complex landscape of disclaimers that vary by local authority. This includes organizations like the FCA in the UK, FINRA in the US, and the ACCC in Australia. Keeping your disclaimers up to date can be challenging, especially if the language isn’t clearly documented within your organization.

Here are some common types of disclaimers needed in advertising and blog content. These should be regularly updated and communicated to marketing teams by your legal or compliance departments to ensure they meet FCA regulations.

- General Past Performance: This disclaimer informs investors that past performance does not guarantee future results, helping to prevent misleading expectations.

- Simulated Past Performance: When illustrating how a product could have performed, firms must base simulations on actual investments or indices and clarify that past performance is not indicative of future results.

- Investment Risk: Disclaimers must advise investors of potential losses and encourage them to consider low-risk options.

- Comparison Rate: This disclaimer provides context for any comparisons made with competitors, noting that prices and fees can vary.

- Performance & Returns: It emphasizes that positive performance is not guaranteed.

- Forecast: A disclaimer that states the information is accurate as of the date provided but is not updated with market changes.

- General Advice Warning: Advises investors that the information may not reflect their specific circumstances and recommends seeking professional advice.

- General Finance: Clarifies that the financial information is for informational purposes only and not financial advice.

- Confidential Material: States that the material is intended for a specific recipient and should not be shared.

- Partnership: Clarifies that communications do not imply a partnership between the parties.

- Logos & Brand: Asserts that logos and brand names are owned by their respective parties and are displayed for identification purposes only.

- Copyright: Claims rights over intellectual property and content on your site.

Key Sections of the FCA Handbook for Marketers

The most critical part of the FCA Handbook for marketers is Chapter 4 of the Conduct of Business Sourcebook (COBS), which outlines rules for financial promotions and communications. Here’s an overview of the most important sections:

COBS 4.2: Fair, Clear and Not Misleading Communications

This section states that financial promotions and communications must abide by the “fair, clear, and not misleading rule.” This rule is designed to ensure consumers are getting what they’ve been promised and that there are no surprises later on.

This rule applies to communications for:

- Customers and potential customers

- Eligible counterparties, which include

- Investment firms

- Credit institutions

- Insurance companies

- Collective investment schemes

- Pension funds or their management companies

- Financial institutions

- National governments, like a public body that deals with public debt at the national level

- Central banks

- Supranational organizations

- Any financial promotion EXCEPT an excluded communication, a non-retail communication, or a third-party prospectus

The expectations are different for different clients. Retail clients require that more information be provided than professional clients or eligible counterparties (listed above).

You must make sure that your financial promotion:

- Discloses risk

- Is transparent about both short- and long-term expectations

- Clearly explains complex structures (especially that benefit the firm)

- Does not falsely lead the client to believe that a statement was endorsed by the FCA or other regulatory body when it was not

- Clearly states if an offered product is not produced by the firm (such as a life insurance policy)

- Does not provide any false guarantee, promise of protection, or security

COBS 4.5: Communicating with Retail Clients (Non-MiFID Provisions)

This section explains the rules of communicating with retail clients, which means a client who is neither a professional client nor an eligible counterparty (listed above) or, in plain English, an inexperienced investor.

A firm must make sure that the information in their communications:

- Includes the name of the firm and date of communication

- Is accurate and transparently represents risks

- Is understandable to the average potential client

- Represents risks in an equal font and layout priority consistent with the rest of the information

- Links the FRN (firm reference number) in the format: “Approver FRN”

- Includes the name of the firm that approved the communication

- Presents comparisons with other businesses in a meaningful and fair way

- Accurately discloses past performance data and does not imply that it is indicative of future performance

COBS 4.5A: Communicating with Clients (Including Past, Simulated Past and Future Performance) (MiFID Provisions)

This section explains the rules for communicating with clients and equivalent parties, which more or less means experienced investors. Your information for clients must include:

- The name of the investment firm

- Consistent font size and layout for disclaimers

- Language understandable by the average member or group it is intended for

- No hidden disclaimers or warnings

Past performance data for clients must cover the past five years and must present that this data is not indicative of future performance. The currency must be clearly stated in this statement, and any commissions, fees, and charges must be clearly disclosed.

Firms must disclose that inherently liquid assets can be hard to sell and, therefore, can lead to delayed result times and tempered results.

COBS 4.6: Past, Simulated Past and Future Performance (Non-MiFID Provisions)

The gist of this section, as you may have gathered from previous sections, is that past performance must be accurately portrayed and cannot be represented as indicative of future performance. In addition to the points in the above section, you must ensure that:

- The most prominent part of your statement is not the fact that you’re making the statement itself. The statement should foremost be informative of accurate past results.

- Simulated past performance must be accurately represented and clearly not indicate future performance.

- Fees, commissions, and charges are accurately disclosed in representations of future performance.

- Risk is accurately reflected.

- Past performance must be displayed in the following format:

Percentage growth

| [Fund name] | Quarter/Year - Quarter/Year | Quarter/Year - Quarter/Year | Quarter/ Year - Quarter/Year | Quarter/ Year - Quarter/Year | Quarter/ Year - Quarter/ Year |

| pgr% | pgr% | pgr% | pgr% | pgr% |

COBS 4.10: Approving and Confirming Compliance of Financial Promotions

This section details how companies are required to have procedures in place to approve communications and financial promotions. Firms must take reasonable steps to approve each communication and must confirm in writing quarterly that existing communications haven’t changed.

Unauthorized individuals cannot communicate a financial promotion. Firms cannot approve communications in person or over the phone—they should be approved in writing to ensure a paper trail.

Firms are responsible for the approval of materials and are not exempt if the materials are claimed to be approved by another firm. The firm must make a reasonable effort to confirm the approval. Firms must also prevent conflicts of interest with their senior management and approval officers.

What Tools Can Help with FCA Regulation?

First up, refer to these resources:

Along with familiarizing yourself with the codes, your greatest tool will be a marketing compliance management platform that uses automation and AI to ensure your materials are within regulation.

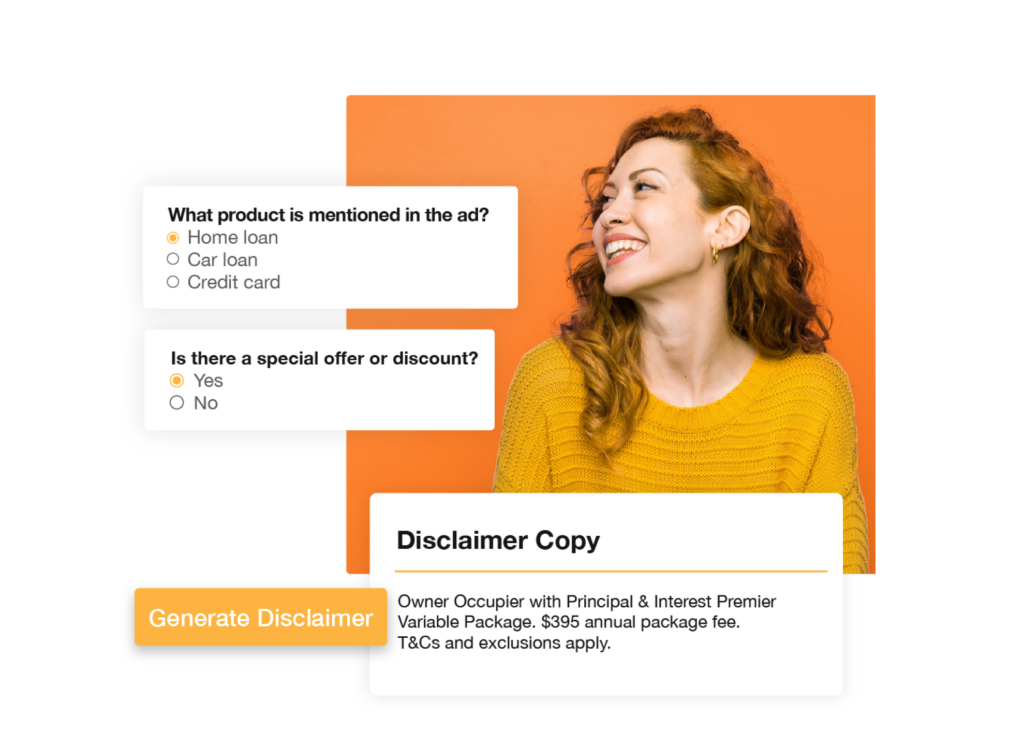

The IntelligenceBank platform not only allows you to brief, create and channel approvals internally, it uses AI to identify non-compliant marketing content. It scans print based material and web pages for compliance red flags in seconds Our RiskGPT functionality then suggests compliant copy options that adhere to FCA, FINRA, and FTC regulations.

If you’d like to discuss how your marketing compliance processes can keep up with FCA regulation, contact us for a demo.

Note: This post is not a substitute for legal or regulatory advice. Always seek professional counsel for compliance-related matters.