Navigating the world of sustainable finance can be tricky for consumers. Many people want to invest their money in a way that benefits the planet, but they often worry about falling prey to greenwashing—the practice of companies making misleading claims about a product’s environmental benefits. In fact, recent surveys show that 64% of investors feel uneasy about this issue, while only 36% believe that financial firms are being upfront and honest about their sustainability efforts.

To tackle these concerns, the UK’s Financial Conduct Authority (FCA) has put forth a set of rules designed to promote transparency and accountability in sustainability claims. If you’re a financial firm, it’s crucial to understand these guidelines as they evolve and prepare for the upcoming enforcement dates that will shape how you communicate your sustainability initiatives.

Let’s explore what’s changing, who it impacts, and why it matters.

What’s the Trouble with Greenwashing?

What are the Updates to Green Guidance in the UK?

In November 2023, the FCA released a comprehensive policy statement titled “Sustainability Disclosure Requirements (SDR) and Investment Labels.” This document emphasized the growing importance of ESG in finance, particularly regarding investments. It highlighted issues such as the lack of standardized information and misleading claims. The SDR aims to ensure that financial products marketed as sustainable genuinely deliver on those claims, backed by robust evidence.

What are the New Greenwashing Rules?

Anti-Greenwashing Rule

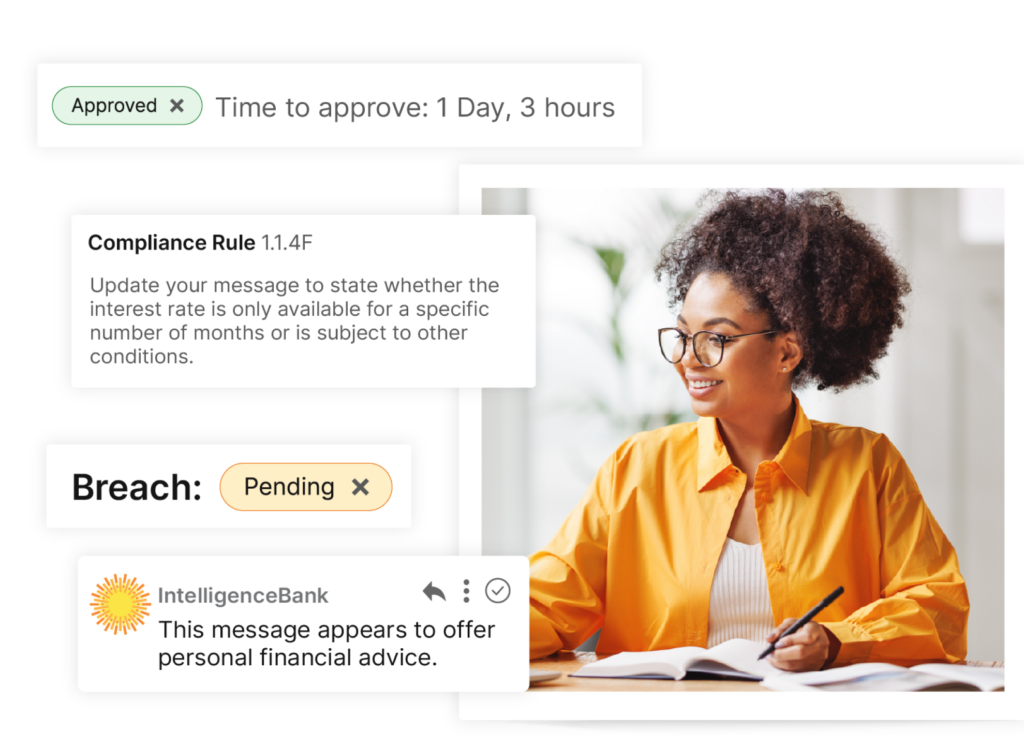

Effective from 31 May 2024, this blanket rule mandates that firms make only “fair, clear, and not misleading” sustainability claims. These claims must align with the actual sustainability profile of the product or service. This rule applies to communications directed at a UK audience, whether retail or commercial, and includes materials made or approved by authorized firms on behalf of unauthorized entities outside the UK.

Investment Labels

Starting from 31 July, firms can begin using one of four new investment labels introduced by the FCA. Each label reflects different sustainability goals and demonstrates a firm’s commitment to responsible investing. These labels are designed to uphold high standards in measurable objectives and how assets are allocated. The four new labels are:

- Sustainability Impact TM

- Sustainability Improvers TM

- Sustainability Focus TM

- Sustainability Mixed Goals TM

- Set clear, specific, and measurable sustainability goals.

- Use strong, evidence-based standards to track their environmental, social, and governance (ESG) performance.

- Ensure that no single asset undermines the overall sustainability objective of the product.

- Allocate at least 70% of a product’s assets in line with the specified sustainability goal before using a label.

Naming and Marketing Rules

Effective from 2 December 2024, the new greenwashing rules regulate the accurate use of sustainability-related terms in product names and marketing materials for retail clients. The use of terms like “green,” “climate,” or “net-zero” is restricted to products bearing one of the new investment labels. If a product lacks an investment label, terms like “sustainable” or “impact” cannot be used without appropriate disclosures.

However, exceptions exist for non-sustainability contexts and factual statements, allowing firms to discuss sustainability in reasonable, non-promotional ways.

Some of the exceptions to the FCA’s greenwashing rules include:

- Non-sustainability contexts: Firms can use still terms like “economic climate” or “financial impact” when not referring to sustainability characteristics.

- Factual statements: Certain non-promotional, factual statements fall outside the scope of this rule. This doesn’t include sustainability-related statements promoted in marketing for product material, which still require disclosures and statements.

Additional Information and Guidelines

The new rules introduce extra communication and disclosure requirements designed to enhance consumer understanding of sustainability features in financial products. These include:

- Consumer-facing Information: Aimed at helping the public understand key sustainability features.

- Pre-contractual and Ongoing Disclosures: For both institutional investors and consumers.

- Distributor Requirements: Ensuring distributors provide complete, up-to-date product information.

Who is Affected?

All Authorized Firms

All Distributors

UK Asset Managers

UK asset managers are expected to familiarize themselves with the requirements in time to implement changes ahead of the communicated deadlines. Considerations include:

- Whether they want to use the new labels.

- Which products, if any, meet each label’s criteria.

- How to update consumer-facing and detailed product-level disclosures accordingly.

- When and how to notify the FCA of label use.

- What needs to happen regarding annual reviews, label changes, etc.

What do Firms Need to Know?

Timing

Each part of the SDR has different timing:

- The anti-greenwashing rule came into effect on 31 May 2024.

- Firms can start using labels on 31 July 2024.

- The naming and marketing rules go into effect on 2 December 2024 but if firms are releasing new offerings before this date, they should consider proactively complying.

Enforcement

While the FCA has clarified that its guidance and examples are not exhaustive and that it won’t be approving steps like label usage, the regulator will still enforce every part of the SDR. This is particularly relevant in three areas:

- Relevance: Firms must know which rules apply to their activities and offerings.

- Timing: The FCA expects compliance as soon as each rule goes into effect; firms shouldn’t wait until these dates to start working on compliance policies and procedures.

- Specifics: Some parts of the SDR, particularly concerning labels, require firms to pay close attention to specific requirements and criteria. Compliance is based at least partially on self-assessment.

How Do I Ensure Compliance?

The SDR is intended to create a more honest, trustworthy, transparent market, which will benefit financial institutions and their clients. However, this means firms like yours will need to reevaluate their offerings and related language.

Step 1: Determine What’s Relevant

Step 2: Choose Your Tools

Multiple teams are involved with the consumer-facing elements of your work, which means they must be part of your SDR compliance efforts. To get the right information to the right people, you need tools that automate and simplify marketing compliance.

As well as increasing accuracy, this greatly reduces back and forth between Legal, Compliance and Marketing teams and allows you to get FCA compliant work to market a lot faster. IntelligenceBank helps you navigate this and other regulatory requirements with confidence — even while juggling different departments’ priorities (such as creativity vs. compliance).

Step 3: Prioritize Consistency and Accuracy

Once your tools are in place, it’s time to ensure consistency and accuracy become priorities in every process. This doesn’t just help you align with SDR requirements when labeling and marketing your products; it also creates a framework for future decision-making, like brainstorming new offerings or campaigns.

Make Compliance Easier Than Ever

The SDR is an important part of the UK’s commitment to a more sustainable future, but it’s certainly not the only requirement in the financial services sector. Organisations need to maintain clear, fair, and trustworthy language in everything they do — and thanks to pressures like regulatory change and interdepartmental conflict, this can be a challenge.

It’s time to leverage technology to automate and scale review processes, empowering your teams and optimizing resources for your organization. Contact us today to see how we can do all this and more.

NOTE: This post isn’t a substitute for legal or regulatory advice; please seek legal counsel on compliance-related issues.