Auto finance firms face a unique compliance challenge: while they provide financing, the marketing of those loans are handled by a vast network of independent auto dealerships.

This decentralized model creates significant risk, as dealers – often unfamiliar with strict financial advertising regulations – may publish non-compliant offers, leaving the finance companies exposed to regulatory penalties.

In this article, we explore how major auto finance providers manage this risk and ensure compliance across thousands of dealer websites and marketing materials – without having direct control over the content.

The Compliance Challenge

Auto finance companies operate in a complex ecosystem where their loans are promoted by:

- Independent dealerships (sometimes numbering in the thousands)

- Third-party agencies that create dealer websites and ads

- Multiple automotive brands (in the case of captive financiers)

The problem? Dealers focus on selling cars, not compliance. Common issues include:

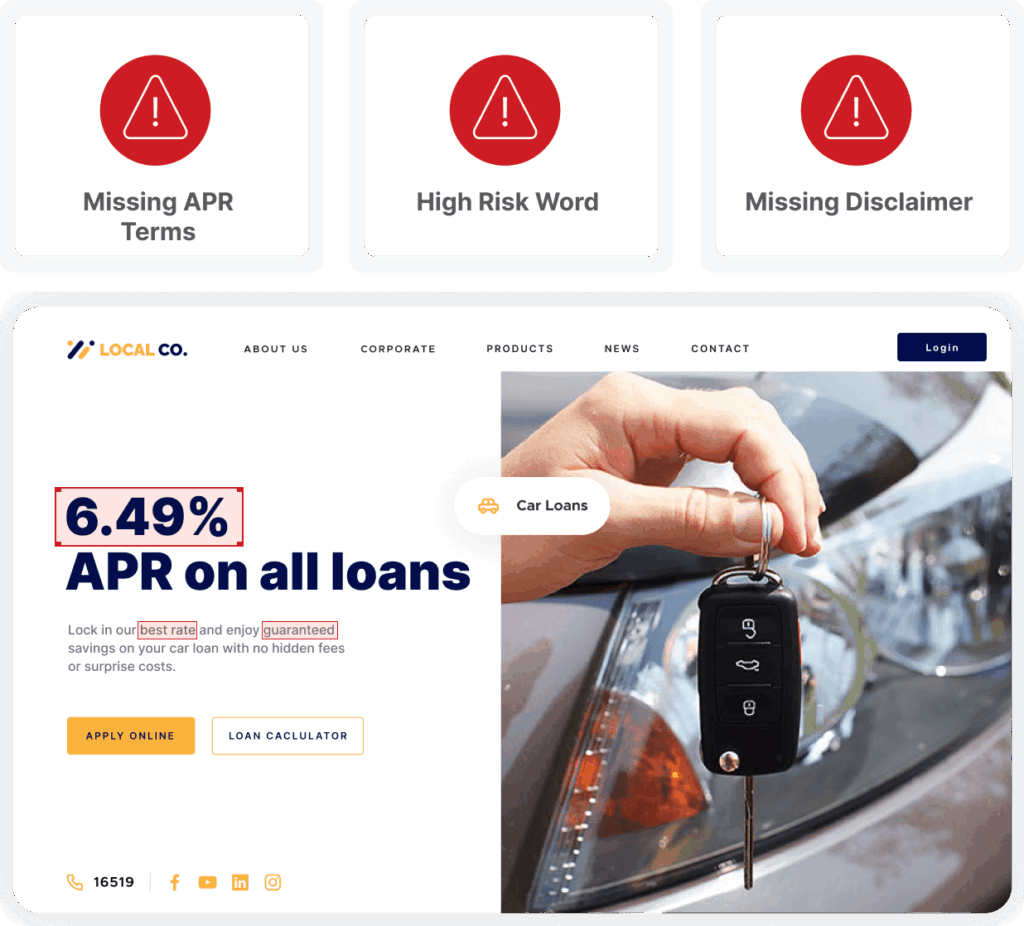

- Omitting mandatory disclaimers

- Using unapproved offers (e.g., ‘Finance pre-approval’)

- Using incorrect interest rate disclosures

- Using non-compliant language (e.g., creating a false sense of urgency)

- Misrepresenting loan terms

- Reusing outdated disclaimers from previous campaigns

And while well intentioned, there is little incentive for dealers to ensure information is flawless as it is not them who bear the wrath of government regulators. That’s right…the legal responsibility falls solely on the finance provider, not the dealer.

A single non-compliant ad could lead to regulatory fines, reputational damage, or even loss of lending licenses. And with regulators now using AI to detect violations, the chances of issues being picked up have skyrocketed.

How Auto Finance Companies Mitigate Risk

Leading finance providers use automated compliance solutions to monitor and enforce marketing standards at scale. Here’s how they do it:

Web Risk Reviews: Scanning thousands of dealer websites

For finance companies with loans marketed across thousands of websites, AI-powered compliance scanning is the only way to detect errors. It is not simply possible to do the task manually. Those who don’t use compliance review technology depend on sporadic random spot checks, which leaves them wide open to incurring a breach notice.

How it works:

- Monthly scans of dealer websites identify pages mentioning the finance brand.

- AI-powered rules check for compliance issues (e.g., missing disclaimers, incorrect APR disclosures).

- Reports flag violations, allowing the finance company to instruct dealers on necessary fixes.

The impact?:

- One major auto financier scans 850,000+ pages annually, catching 45,000+ potential risks— that’s 5% of all pages reviewed.

- Without automation, manual reviews would take hundreds of years of human effort—making compliance at this scale impossible.

Content Risk Reviews: Ensuring Print & Digital Campaigns Are Compliant

For financiers that promote their own offers through various owned vehicle brands, the challenge is a little different. Their marketing teams must approve every marketing campaign to ensure compliance before publication.

How it works:

- AI reviews marketing materials (brochures, digital ads, emails) against dynamic compliance rules.

- Checks include:

- Correct disclaimers for specific campaigns (e.g., guaranteed future value vs. standard loans)

- Accurate interest rates and comparison rates

- Properly formatted legal text

- Marketing teams receive instant feedback, speeding up approvals while reducing compliance risks.

The benefit? Faster, more efficient compliance reviews that cut out weeks of back-and-forth between brand marketing and legal.

How the FTC’s 2024 CARS Rule Intensifies Compliance Risks

For auto finance companies operating in the US, the FTC’s new regulations target deceptive dealership practices, but auto finance providers face ripple effects because:

1. Stricter Pricing Transparency Requirements:

- Dealers must now provide “all-in” pricing (including mandatory add-ons) in any ads mentioning payment terms

- Finance implications: Any dealer ad promoting financing must now clearly disclose:

– Total vehicle cost (no hiding fees in fine print)

– If add-ons are required for financing approval

– How down payments affect monthly payments

So, if your dealers run non-compliant ads (e.g., “$299/month!” without disclosing $5,000 mandatory down payment), you share liability.

2. Explicit ban on misleading “discount” claims:

Dealers can’t advertise “discounted” APRs unless:

- The rate is truly below market average

- All qualifying restrictions are disclosed upfront

Common violation caught that can be caught in scans: Dealers advertising “special 2.9% financing” without revealing:

- Only applies to 720+ credit scores

- Requires 48-month term

3. New record keeping burdens

- Dealers must retain all marketing materials for 24 months.

Finance providers should:

- Archive dealer ads mentioning their financing

- Document all compliance corrections (proof of due diligence)

How automated compliance reviews address these changes

The CARS Rule makes your existing web scanning even more valuable by:

- Flagging “All-in Pricing” Violations

- AI can detect when payment terms lack:

- Mandatory fee disclosures

- Down payment requirements

- AI can detect when payment terms lack:

- Identifying Fake “Discounts”

- Rules can check if:

- Advertised APRs match finance provider’s approved rates

- Qualifying footnotes are present and accurate

- Rules can check if:

- Creating Audit Trails

- Monthly scans automatically document:

- When violations were found

- When dealers were notified

- If/when fixes were implemented

- Monthly scans automatically document:

Lessons from the Field: What Works

Insights from real-world implementations reveal best practices:

Proactive monitoring beats reactive firefighting

Companies that scan dealer sites monthly reduce errors by 60%+ year-over-year by catching mistakes early. Those relying on random spot checks face a higher prospect being fined.

Education improves dealer compliance

Some finance providers supplement scanning with:

- Dealer training (explaining compliance rules)

- Pre-approved templates (for websites/ads)

Technology scales better than humans

One team reduced compliance workload by 80% by replacing manual reviews with AI, freeing staff for more strategic risk management.

The Hidden Costs of Non-Compliance in Auto Finance

Many finance providers underestimate the full impact of marketing violations:

- Regulatory fines (recent cases show penalties exceeding $10M for repeat offenders)

- Operational disruptions (forced campaign takedowns during peak sales periods)

- Dealer relationship strain (constant correction requests damage partnerships)

- Lost competitive edge (competitors gain trust while you face scrutiny)

The Bottom Line: Compliance Doesn’t Have to Slow Sales

Auto finance providers want to get people into cars. And they want their dealers to be successful. While they can’t control every dealer’s marketing, they don’t want to slow down the sales process. That’s why they enforce compliance through:

- Automated AI web scanning (catching dealer website violations)

- AI-powered content reviews (ensuring brand campaigns meet regulations)

With fines for non-compliance reaching millions per violation, proactive monitoring isn’t just best practice, it’s a financial necessity. If you’d like more information or a live, customised demo please drop us a line.

This article is based on real-world challenges faced by auto finance providers. Names have been omitted for confidentiality.