Regulation P is a federal U.S. regulation that implements the privacy provisions of the Gramm-Leach-Bliley Act (GLBA). It requires banks, credit unions, and other financial institutions to protect nonpublic personal information (NPI), giving consumers the right to know how their data is collected and shared. It is also used to limit certain types of sharing with third parties.

For Marketing and Marketing Compliance teams at financial institutions, Regulation P shapes how consumer-facing marketing content should be structured across every channel. Emails, digital ads, direct mail and branch collateral all need to reflect its requirements. This guide explains what Regulation P requires, who it applies to, the risks of non-compliance and how marketing teams can build a more efficient review process.

For a broader introduction to marketing compliance in financial services, see our marketing compliance guide.

At-a-Glance: Regulation P

| Full Name | Privacy of Consumer Financial Information (Regulation P). |

| Authorizing Statute | Gramm-Leach-Bliley Act (GLBA), 15 U.S.C. § 6801 et seq. |

| Primary Regulator | Consumer Financial Protection Bureau (CFPB); also enforced by FTC, OCC, Federal Reserve and state regulators. |

| Applies To | Banks, credit unions, mortgage lenders, securities firms, insurance companies and other financial institutions offering consumer financial products or services. |

| Protects | Nonpublic personal information (NPI) of consumers including account numbers, income data, credit history, SSNs and transaction records. |

| Key Requirements | Initial and annual privacy notices; opt-out rights for NPI sharing with nonaffiliated third parties; data safeguards. |

| Penalties | Up to $1 million per day for violations plus reputational and legal exposure. |

What Is Regulation P?

Regulation P is a federal privacy regulation that governs how U.S. financial institutions collect, use and share the nonpublic personal information (NPI) of their consumers. It was issued to implement Title V of the Gramm-Leach-Bliley Act (GLBA) and was originally administered by the Federal Reserve Board before transferring to the Consumer Financial Protection Bureau (CFPB) in 2011 under the Dodd-Frank Act.

NPI is any personally identifiable financial information that a consumer provides to a financial institution that results from a transaction with the institution or that the institution otherwise obtains. Examples of this include Social Security numbers, bank account numbers, income and credit history, transaction records and loan application data. Information that is publicly available, (such as a name listed in a phone directory), is not NPI.

A critical distinction under GLBA and Regulation P is the difference between a consumer and a customer. A consumer is any individual who obtains or has obtained a financial product or service for personal, family or household purposes. A customer is a consumer who has an ongoing relationship with the institution, for example, a checking account holder. This matters because customers are entitled to annual privacy notices, while one-time consumers may only be entitled to an initial notice at the point of transaction.

Regulation P is enforced by multiple regulators depending on institution type: the CFPB and FTC for most financial institutions, the OCC for national banks, the Federal Reserve for state member banks and state regulators for certain other entities.

What Does Regulation P Require?

Regulation P imposes three core obligations on covered financial institutions: providing privacy notices, offering opt-out rights and implementing data safeguards. Each has direct implications for how marketing content is created and reviewed.

1. Privacy Notice Requirements Under Regulation P

Financial institutions should provide consumers with clear and conspicuous privacy notices explaining what NPI is collected, how it’s used, with whom it is shared and how consumers can limit certain sharing.

There are three notice types:

| Notice Type | When Required | Key Contents |

|---|---|---|

| 1. Initial Privacy Notice | At the time a customer relationship is established | Categories of NPI collected; categories of NPI disclosed; categories of third parties receiving NPI; opt-out rights and how to exercise them; data protection practices |

| 2. Annual Privacy Notice | Once per year for each customer with an ongoing relationship | Same as initial notice; should reflect current practices |

| 3. Revised Privacy Notice | Before the institution materially changes its privacy practices | Updated disclosure of new sharing practices; revised opt-out instructions |

Important: The Fixing America’s Surface Transportation (FAST) Act, enacted in 2015, created an exception to the annual notice requirement. Institutions are not required to send an annual notice if they have not changed their privacy policies since the last notice and they do not share NPI with nonaffiliated third parties in ways that trigger opt-out rights. Many institutions qualify for this exception, but it requires active assessment each year.

Regulation P also provides a model privacy form that institutions may use. Using the model form creates a safe harbor for compliance with the notice content and format requirements.

2. Opt-Out Rights Under Regulation P

Consumers have the right to opt out of having their NPI shared with nonaffiliated third parties—meaning companies that are not affiliated with the financial institution. Institutions should provide a reasonable means of opting out, such as a toll-free number, reply form, or electronic method.

Key exceptions apply. Institutions may share NPI with nonaffiliated third parties without providing opt-out rights in the following circumstances:

- Service providers and joint marketing: Sharing is permitted when the third party is performing services on behalf of the institution under a contract.

- Transactions and servicing: Sharing necessary to process or service a financial product or service requested by the consumer.

- Fraud prevention and legal compliance: Sharing required to protect against fraud, comply with legal requirements or respond to legal process.

Joint account holders should each be given an opportunity to opt out and an opt-out by one holder does not automatically apply to others.

3. Data Safeguard Requirements Under Regulation P

Regulation P requires institutions to maintain administrative, technical and physical safeguards to protect NPI from unauthorized access, use or disclosure. These protections apply to both physical records and digital data.

Account number restrictions are particularly relevant for marketing teams. Regulation P prohibits financial institutions from disclosing account numbers or similar access codes to nonaffiliated third parties for use in telemarketing, direct mail marketing or electronic marketing – even if the consumer has not opted out. This restriction applies regardless of whether the sharing would otherwise be permitted.

Institutions are also prohibited from redisclosing or reusing NPI received from another financial institution in ways that are not permitted by the original institution’s privacy notice.

Who Does Regulation P Apply To?

Regulation P applies to financial institutions that offer financial products or services to consumers for personal, family or household purposes. Covered institution types include:

- Banks and savings associations

- Credit unions

- Mortgage lenders and brokers

- Securities firms and investment advisors

- Insurance companies offering consumer products

- Finance companies and auto lenders

- Financial advisors and planners

Regulation P does not apply to business accounts. The regulation protects consumers, (individuals obtaining financial products for personal use), not businesses or commercial entities. If a financial institution offers both consumer and business products, Regulation P applies only to the consumer-facing side.

For Marketing and Marketing Compliance teams, this scope determination matters practically. Consumer-facing campaign materials — emails, digital ads, direct mail, branch collateral and landing pages — should be reviewed for compliance with Regulation P notice and opt-out requirements. Business-to-business marketing materials are not subject to the same requirements, though other regulations may apply.

Financial institutions operating across multiple product lines and regions face particular complexity here, as the line between consumer and commercial communications is not always straightforward in practice. IntelligenceBank’s banking and finance compliance capabilities are designed specifically for these environments, helping Marketing and Marketing Compliance teams manage content review across consumer-facing channels with consistency and speed.

What Is the Difference Between GLBA and Regulation P?

The Gramm-Leach-Bliley Act (GLBA) is the U.S. federal statute; Regulation P is the implementing regulation that gives the law its operational requirements. Think of GLBA as the law and Regulation P as the rulebook that financial institutions should actually follow.

| Dimension | GLBA | Regulation P |

|---|---|---|

| Type | Federal statute (law passed by Congress) | Federal regulation (implementing rule issued by regulators) |

| Enacted/Issued | Enacted in 1999 | Originally issued by the Federal Reserve; transferred to CFPB in 2011 |

| Scope | Broader — includes financial privacy, safeguards and pretexting provisions | Narrower — specifically implements the financial privacy provisions of GLBA |

| Enforced by | Multiple agencies depending on institution type | CFPB (primary), FTC, OCC, Federal Reserve, state regulators |

What Are the Risks of Non-Compliance with Regulation P?

Non-compliance with Regulation P creates financial, reputational, regulatory, and legal risk—all of which can be triggered by failures in marketing content as much as by failures in back-office processes.

Financial Penalties: The CFPB has authority to impose civil penalties for Regulation P violations. Penalties can reach up to $1 million per day depending on the severity and nature of the violation. The FTC and state regulators also have enforcement authority and can impose their own fines.

Reputational Damage: Public enforcement actions erode consumer trust quickly. In financial services, where trust is the foundation of customer relationships, a publicized Regulation P violation can accelerate customer attrition and damage long-term brand equity in ways that outlast the regulatory action itself.

Increased Regulatory Scrutiny: Institutions that breach Regulation P often face heightened examiner attention such as more frequent audits, expanded scope of review and in some cases formal consent orders that impose ongoing reporting obligations and restrict business activities.

Legal Action: Consumers whose NPI is improperly shared may pursue private legal action, including class action lawsuits. The reputational exposure from litigation compounds the direct legal costs.

For marketing leaders, the practical implication is that marketing content is a meaningful source of Regulation P risk. Missing a required privacy disclosure in an email campaign or distributing an account number in a direct mail piece are exactly the kinds of errors that surface in examinations and enforcement actions. The right marketing compliance software can reduce that exposure systematically.

Key Marketing Compliance Challenges Under Regulation P

Regulation P creates specific marketing compliance challenges that generic compliance frameworks don’t fully address. Marketing teams at financial institutions face a set of pressures that sit at the intersection of content volume, campaign speed and regulatory precision.

- Content volume and channel proliferation: Marketing content volume has risen 85% year-on-year, and for financial institutions, every piece of that consumer-facing output spans multiple channels (e.g., emails, social media, digital ads, direct mail, and branch collateral). With each requiring Regulation P review, it becomes an overwhelming task to manage approvals manually.

- Privacy disclosures in marketing materials: Knowing when a privacy notice is required and how to format it correctly across different channels and content types is not straightforward. Getting this wrong, (even unintentionally), creates regulatory exposure.

- Campaign speed vs. review bottlenecks: Marketing teams operate under tight deadlines. Regulation P review adds time to the production cycle and without a structured process, compliance checks become the bottleneck that delays campaign launches.

- Inconsistent reviewer interpretations: When multiple Marketing Compliance Reviewers assess similar content, they don’t always reach the same conclusions or risk thresholds. Inconsistency creates compliance gaps and erodes trust between marketing and compliance teams.

- Keeping pace with regulatory updates: Regulation P requirements continually evolve and most marketers are not compliance specialists. Staying current and ensuring that review rules, disclaimers and privacy notices reflect the latest requirements is an ongoing challenge.

None of these challenges are insurmountable, but they do compound quickly when content volume is high and review processes are manual. Addressing them requires a structured approach—one that builds Regulation P requirements into the content workflow rather than applying them as a final gate before launch. Our guide to what is marketing compliance covers the broader framework that financial services marketing teams operate within.

How AI Monitors Digital Banking Channels for Privacy Compliance

Retail bank websites, email programs, and social media channels are among the most common surfaces where Regulation P privacy obligations must be maintained, and they are also among the hardest to monitor manually. Privacy notices, opt-out mechanisms, and data collection disclosures that were compliant at launch can drift out of compliance as pages are updated, campaigns change, or new content is published without a full privacy review. AI-powered web and social media risk reviews address this by continuously scanning published digital content for privacy-related compliance gaps, such as missing or outdated opt-out language, privacy notices that no longer reflect current data practices, and consumer-facing pages that reference discontinued products or expired terms.

For banks with branch networks, partner channels, or third-party distribution relationships, the monitoring challenge is even more complex. Each external channel may publish consumer-facing content that carries the bank’s privacy obligations, but central compliance teams have limited visibility into what appears on those properties. AI-powered monitoring tools can extend compliance scanning across these distributed digital channels, flagging privacy compliance issues on partner websites and social accounts alongside the bank’s own properties, so that Regulation P requirements are maintained wherever consumer data is being discussed or collected.

How To Streamline Regulation P Marketing Compliance

The most effective response to Regulation P’s marketing compliance demands is a structured, automated review process that catches common errors before content reaches a human reviewer. And, importantly for audit purposes, one that maintains an auditable record of every review decision.

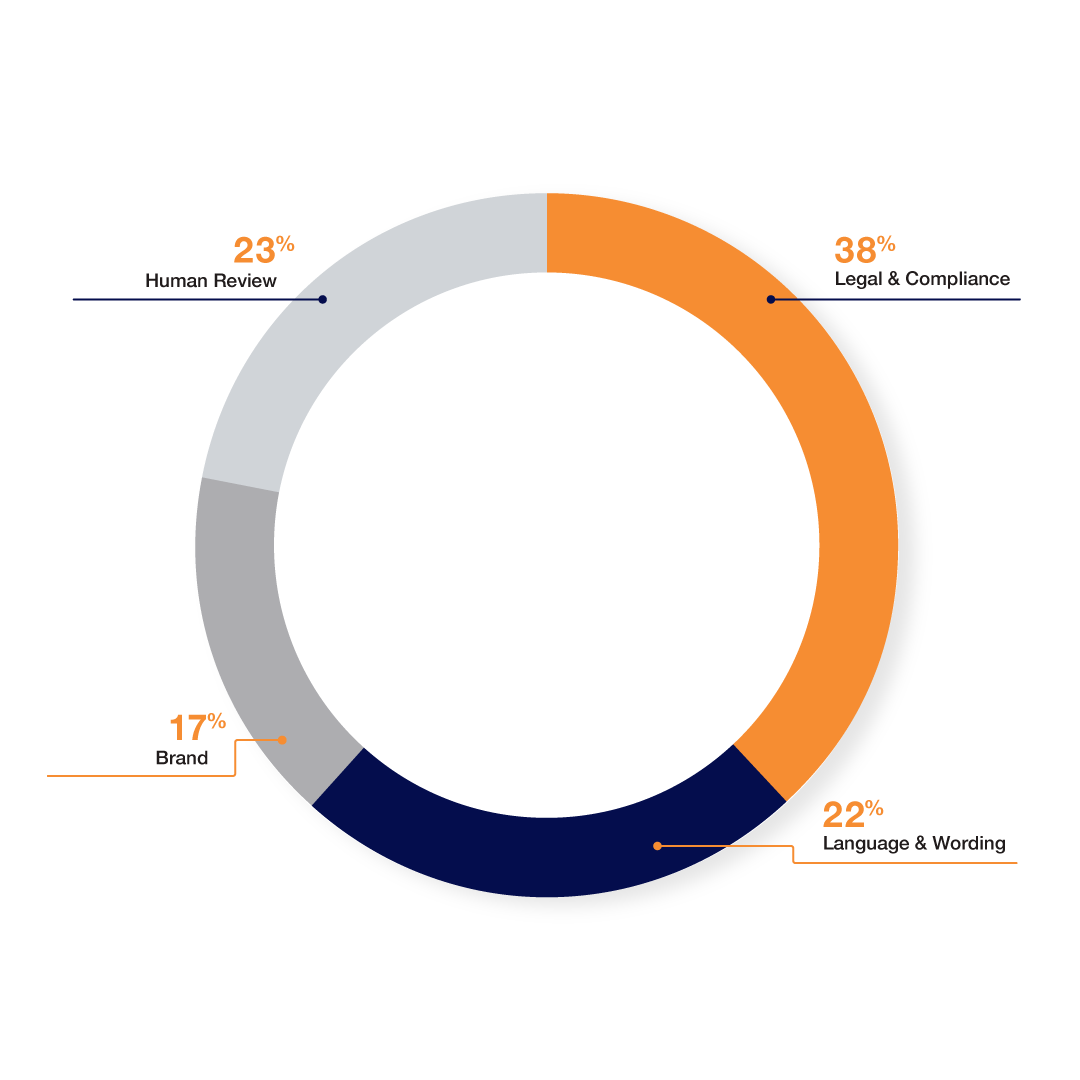

Based on IntelligenceBank customer data, more than 75% of comments on marketing content made by Legal or Marketing Compliance teams relate to errors that AI can identify automatically. The breakdown by comment type:

- 38% relate to legal and marketing compliance issues: outdated disclaimers, inaccurate claims, missing disclosures and incorrect regulatory language.

- 22% relate to wording: phrasing issues around claims and product disclosures.

- 17% relate to brand compliance: logo usage, font sizes, tone and readability.

- 23% required direct human review: nuanced or context-specific judgment calls.

This means that for most financial institutions, the majority of Regulation P review effort is being spent on errors a well-configured automated review could catch on submission.

How Automated Compliance Reviews Work

Content Risk Reviews

Content Risk Reviews operate through a straightforward workflow.

- Marketing content—such as ads, emails, PDFs, landing pages, and social posts—is submitted for review.

- Configured rules check the content against Regulation P requirements: privacy notice inclusion, opt-out mechanism presence, account number restrictions and disclaimer accuracy.

- Issues are flagged with specific feedback before the content reaches a human reviewer.

IntelligenceBank’s risk detection capabilities include industry-specific risk rule libraries pre-configured for Regulation P and other banking regulations. These libraries can be deployed as-is or customized to reflect an institution’s specific policies and practices. The platform also maintains a complete audit trail of all review activity which is essential for demonstrating compliance during audit.

Disclaimer Engine

The Disclaimer Engine automates the generation and placement of required disclosures, reducing the risk of a privacy notice being omitted or incorrectly formatted across different content types and channels.

Results from Automated Regulation P Reviews

For institutions managing high volumes of consumer-facing marketing content, the efficiency gains from automated reviews are significant. To estimate what a structured review process could save your team, use the compliance review ROI calculator.

Regulation P Compliance Checklist for Marketing Teams

This checklist covers the key Regulation P requirements that apply to consumer-facing marketing content. It is designed as a pre-launch review framework rather than a substitute for legal review and provides a structured starting point for Marketing and Marketing Compliance teams.

- Privacy notice included: All consumer-facing marketing materials that trigger notice requirements include a clear and conspicuous privacy notice explaining what NPI is collected, how it is used and with whom it is shared.

- Opt-out mechanism present and accessible: Any communication involving NPI sharing with nonaffiliated third parties includes a functional opt-out mechanism (toll-free number, reply form or electronic method) that is prominently displayed and easy to use.

- Opt-out accessible to joint account holders: Where the communication relates to joint accounts, each account holder has an independent opportunity to opt out.

- Account number restrictions observed: No account numbers, credit card numbers or similar access codes are disclosed to nonaffiliated third parties in direct mail, email or other marketing communications, (regardless of opt-out status).

- NPI handling confirmed: Any NPI referenced or used in the campaign has been obtained and is being used in a manner consistent with the institution’s current privacy notice and Regulation P’s permitted disclosure categories.

- Third-party data attribution verified: Any third-party data used in the campaign is sourced and used in a manner consistent with Regulation P’s service provider and joint marketing exceptions and is covered by an appropriate contractual agreement.

- Disclaimer accuracy confirmed: All disclaimers and required disclosures reflect current regulatory language and have been verified against the institution’s most recent privacy notice.

- Joint marketing agreements reviewed: Any joint marketing arrangement with a nonaffiliated financial institution has been reviewed to confirm it meets Regulation P’s requirements for permissible sharing.

- Record-keeping requirements met: All review decisions, approvals and compliance sign-offs are documented and retained in a format accessible for examination purposes.

- Annual privacy notice exception assessed: If the institution is relying on the FAST Act annual notice exception, eligibility has been confirmed for the current year which means no material policy changes have occurred and no sharing triggers opt-out rights.

Frequently Asked Questions About Regulation P

What is Regulation P?

Regulation P is a federal U.S. regulation that implements the privacy provisions of the Gramm-Leach-Bliley Act (GLBA). It requires financial institutions to provide consumers with privacy notices explaining how their nonpublic personal information (NPI) is collected, shared and protected. It gives consumers the right to limit certain types of sharing with nonaffiliated third parties and is administered primarily by the Consumer Financial Protection Bureau (CFPB).

What law does Regulation P implement?

Regulation P implements Title V, Subtitle A of the Gramm-Leach-Bliley Act (GLBA), which was enacted by U.S. Congress in 1999. GLBA is the broader statute; Regulation P is the specific implementing regulation that defines the operational requirements financial institutions should follow to comply with GLBA’s privacy provisions.

Does Regulation P apply to business accounts?

No. Regulation P applies only to consumer financial products and services i.e., those obtained by individuals for personal, family or household purposes. It does not apply to business or commercial accounts. Financial institutions that serve both consumers and businesses should apply Regulation P requirements only to their consumer-facing marketing content and communications.

What types of information does Regulation P protect?

Regulation P protects nonpublic personal information (NPI) – any personally identifiable financial information provided by a consumer to a financial institution, resulting from a transaction with the institution or otherwise obtained by the institution. Examples include Social Security numbers, account numbers, income data, credit history, transaction records and loan application information. Publicly available information is not considered NPI.

Are banks still required to send annual privacy notices?

Not always. The FAST Act (2015) created an exception to the annual notice requirement. Financial institutions are not required to send annual notices if they have not changed their privacy practices since the last notice and they do not share NPI with nonaffiliated third parties in ways that trigger opt-out rights. Institutions that do share NPI in those ways, (or that have changed their policies), should still send annual notices.

How can consumers opt out under Regulation P?

Consumers have the right to opt out of having their NPI shared with nonaffiliated third parties. Financial institutions should provide a reasonable opt-out method such as a toll-free number, a reply form or an electronic mechanism. They should also give consumers a reasonable period to opt out before sharing begins. Certain sharing is exempt from opt-out rights, including sharing with service providers under contract and sharing necessary to complete a transaction.

What are the penalties for violating Regulation P?

Civil penalties for Regulation P violations can reach up to $1 million per day depending on the severity of the violation, under the CFPB’s enforcement authority. The FTC and state regulators also have authority to impose separate penalties. Beyond financial penalties, violations can result in consent orders, reputational damage, increased regulatory scrutiny and private legal action including class action lawsuits.

Who enforces Regulation P?

Regulation P is enforced by multiple regulators depending on institution type. The CFPB has primary enforcement authority over most covered financial institutions. The FTC enforces Regulation P for entities not subject to CFPB oversight. The OCC enforces it for national banks, the Federal Reserve for state member banks and state regulators for certain other covered entities.

Does Regulation P apply to mortgage companies?

Yes. Mortgage lenders and brokers that offer consumer mortgage products are covered by financial institutions under Regulation P. They should provide initial privacy notices to consumers at the time of application or when the mortgage relationship is established, comply with opt-out requirements for NPI sharing and maintain required data safeguards. The same requirements apply to consumer auto lenders and other non-bank financial institutions offering consumer credit products.

How can marketing teams ensure compliance with Regulation P?

The most reliable approach combines a clear internal review process with automated content review capabilities. Marketing and marketing compliance teams should establish pre-launch checklists covering privacy notice inclusion, opt-out mechanism presence, account number restrictions, and disclaimer accuracy. Automated content risk reviews can flag common Regulation P issues before content reaches a human reviewer, therefore reducing review time and the risk of errors reaching the market. Learn more about marketing compliance software designed for regulated financial institutions.

Ready to reduce Regulation P review time and risk? Book a Demo or explore IntelligenceBank’s banking and finance compliance capabilities.

Disclaimer: This document is not intended as a substitute for legal advice. It has been prepared by IntelligenceBank, a provider of marketing compliance software. Financial institutions should seek professional legal and regulatory advice when establishing internal compliance protocols.