AI marketing compliance software is a purpose-built platform that automatically reviews marketing content — from digital banner ads and product disclosure statements to social posts and co-branded partner materials — against regulatory, legal and brand requirements before publication, and monitors live content on an ongoing basis after it goes live. For Australian banks, superannuation funds and wealth managers, this category of software addresses a problem that manual review processes can no longer solve at scale: the intersection of high content volume, accelerating regulatory complexity and the near-zero tolerance for error that characterizes financial services marketing in Australia.

Understanding how AI marketing compliance software works — and how to deploy it across the full content lifecycle — is now central to building a marketing operation that can move at market speed without exposing the organization to regulatory risk. This guide covers the regulatory frameworks that govern financial services marketing in Australia, the three operational phases where AI compliance checks deliver the greatest impact, and how to build the business case for automation.

Here’s what you’ll learn:

- The definition of marketing compliance and why content volume is the core scaling problem

- The ASIC, APRA, ACCC and ACMA regulations governing financial marketing in Australia

- How AI risk detection works inside Word, PowerPoint, Figma and Canva at the point of creation

- How automated review workflows compress approval cycles from days to hours

- How continuous post-publication monitoring covers websites, ads, social channels and partner networks

- How to measure the ROI of marketing compliance automation

- How to get started with IntelligenceBank for Australian financial services

What Is Marketing Compliance for Financial Services in Australia?

Marketing compliance for financial services is the systematic process of ensuring that every piece of marketing content meets the legal, regulatory and brand requirements that govern how financial products are promoted to Australian consumers. This spans everything from a home loan comparison landing page and a superannuation performance table to a co-branded insurance brochure and a social media rate offer. In a sector where a single misleading claim can trigger regulatory action, reputational damage or a multi-million dollar penalty, compliance is not optional — it is operational infrastructure.

For Australian financial services organizations, the compliance challenge has intensified sharply in recent years. Marketing teams are producing more content across more channels than at any previous point. A mid-tier retail bank might review several hundred pieces of marketing collateral per month. A large superannuation fund with multiple investment options, insurance products and member communications across digital and print could easily review more than a thousand individual creative assets every month. According to Tessa Court, CEO of IntelligenceBank: “We are seeing our customers across financial services double or even triple the amount of content they are creating and storing with us. This is largely due to AI-generated content. To truly scale content operations, it is impossible to stay on top of the approval process without using AI to automatically check it.”

The volume and velocity problem

The problem is not just volume — it is also velocity. Regulatory requirements change. Interest rates move. Product features are updated. Offers expire. A homepage banner that was compliant last quarter may inadvertently display an outdated comparison rate today. Manual compliance review cannot keep pace with this rate of change, and the risk of a gap is not theoretical: ASIC, APRA and the ACCC have all demonstrated willingness to take action against financial services firms for marketing breaches in recent years.

- Content volume: A mid-tier retail bank may review several hundred pieces of collateral per month; a large super fund can exceed a thousand assets.

- Content velocity: Rates, product terms and regulatory guidance change continuously — manual review cannot keep pace.

- Channel proliferation: Digital-first marketing has multiplied the number of channels requiring active monitoring, from websites and social media to broker partner sites.

- Partner network risk: Distribution partners such as mortgage brokers and financial advisers operate their own marketing materials, creating compliance exposure outside the organization’s direct control.

What Are the Key Regulations for Marketing Financial Products in Australia?

Australian financial services marketing sits at the intersection of four major regulatory frameworks. Understanding the obligations under each — and how they interact — is the starting point for building an effective compliance program. The table below summarizes the key requirements relevant to marketing teams.

| Regulator | Focus Area | Key Marketing Obligations | Penalty (max) |

|---|---|---|---|

| ASIC | Financial promotions & advice | Content must be accurate, balanced and not misleading. Includes digital ads, social media, websites, email campaigns and PDFs. Product disclosure statements must be prominently displayed. Unlicensed financial product advice is prohibited. | Up to $1.565M per contravention (corporates) |

| APRA | Prudential governance & product marketing | Superannuation funds must ensure all member communications meet best financial interests duty. Marketing for insurance and banking products must not overstate performance or understate risk. Requires documented approval processes. | Enforceable undertakings; licence conditions; referral to ASIC |

| ACCC / ACL | Consumer protection & false claims | Prohibits misleading or deceptive conduct under the Australian Consumer Law (ACL). Applies to all financial product advertising. Comparisons, testimonials and interest rate claims must be accurate and substantiated. | Up to $50M per contravention (corporates) |

| ACMA | Digital & broadcast advertising | Regulates financial advertising across broadcast, online and digital channels. Spam Act compliance required for email marketing. Do Not Call Register must be respected. Telemarketing scripts for financial products must meet disclosure standards. | Up to $2.23M per contravention for spam breaches |

What the combined obligations mean in practice

The combined effect of ASIC, APRA, ACCC and ACMA obligations means that marketing teams must satisfy multiple — sometimes overlapping — compliance requirements for a single piece of content. A home loan campaign landing page, for example, must display the comparison rate with a standardized ASIC warning statement, ensure all headline claims are accurate and not misleading under the ACL, align with responsible lending representations under APRA, and meet Spam Act and privacy requirements if the page drives email or SMS lead capture. AI marketing compliance software addresses this by encoding these requirements as machine-readable rules that can be customized to a company’s risk tolerance and run automatically, at production speed, every time.

How Does AI Marketing Compliance Software Work at the Point of Content Creation?

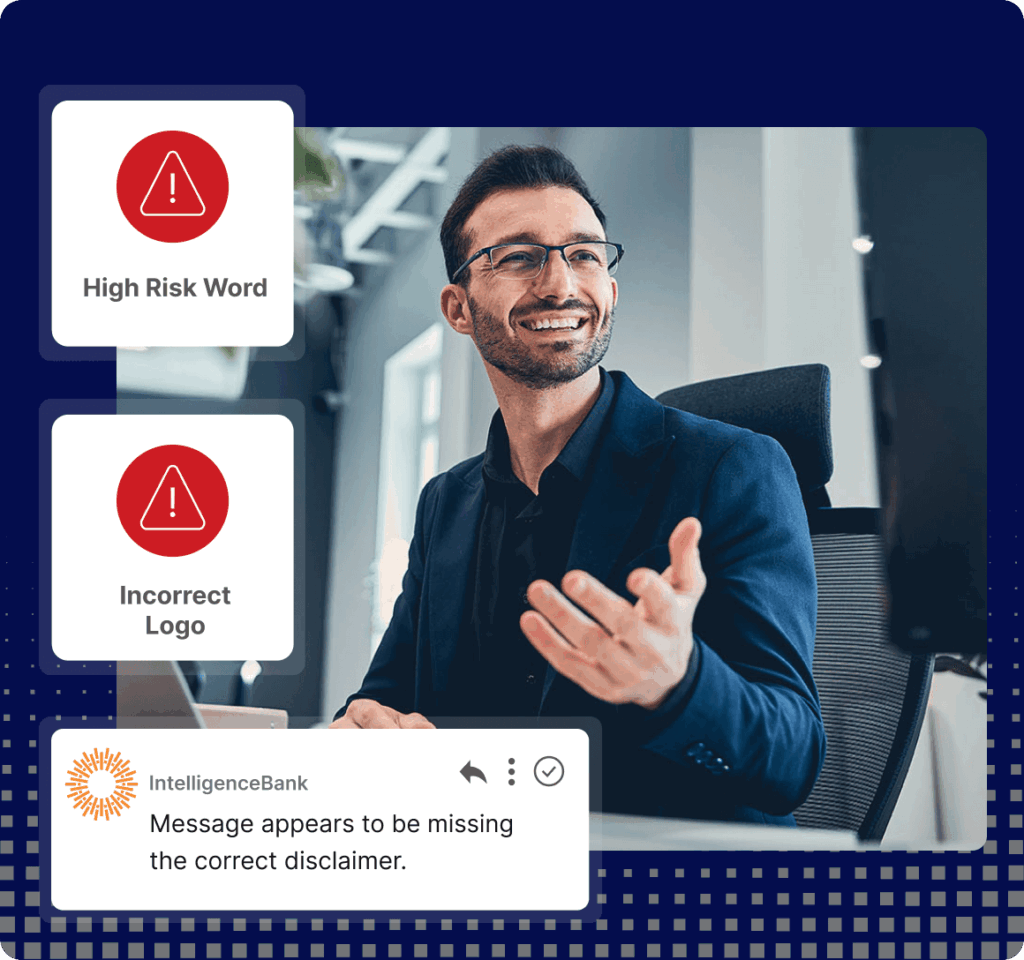

The most efficient place to catch a compliance issue is before it is ever submitted for review. IntelligenceBank’s compliance platform integrates directly with the tools that Australian financial services marketing and design teams use every day — Microsoft Word, PowerPoint, Figma, Canva and more — through native plugins and a browser extension. As content is being authored, the AI risk detection engine runs in the background, checking the work against a library of custom risk rules built in collaboration with the organization’s legal, compliance and brand teams.

These rules can be configured to reflect the specific obligations of the business — whether that is ASIC Regulatory Guide 234 (RG 234) requirements for rate advertising, APRA CPS 234 implications for digital communications governance, or internal brand standards such as the required use of approved disclaimers and mandatory font sizes for disclosure text. By surfacing issues at the point of creation with inline risk flags, IntelligenceBank eliminates the rework cycles that occur when compliance issues are discovered at the review stage.

Common rule types deployed by financial services organizations

The types of AI risk rules that Australian financial services organizations typically configure include:

- Prohibited language detection: Flags superlatives such as “best,” “lowest” or “guaranteed” that are prohibited or restricted in financial advertising without substantiation.

- Mandatory disclosure checks: Verifies that required disclaimer text, comparison rate warnings or product risk disclosures are present and prominent.

- Legibility standards: Checks that disclosure text meets minimum font size requirements for print and digital formats.

- Numeric accuracy flags: Identifies numbers, percentages and dollar amounts that require verification or contextual substantiation.

- Offer expiry detection: Highlights time-limited offers or promotional rates that may require an explicit validity period.

- Partner co-brand compliance: Ensures third-party co-branded materials include required regulatory notices.

IntelligenceBank helped reduce marketing compliance reviews to two minutes per document.

IntelligenceBank customer, financial services sector

How Do Automated Approval Workflows Speed Up Compliance Sign-Off?

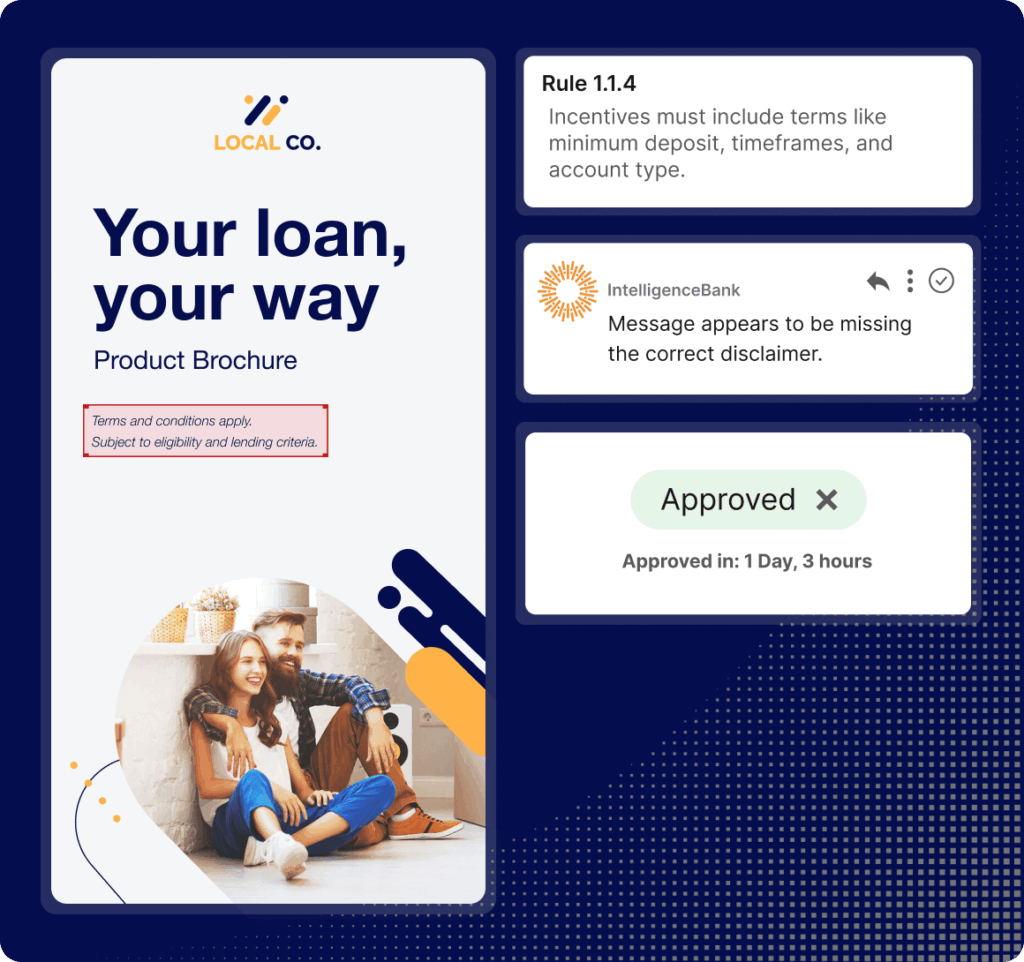

Even with upstream risk detection in place, content must still pass through a formal review and approval process before publication. IntelligenceBank’s integrated workflow platform removes the bottlenecks that make compliance review the most common cause of content production delays in financial services organizations. When content enters the review workflow, the platform automatically runs a compliance risk scan and generates a risk score so reviewers know immediately where to focus their attention.

The platform supports parallel approval workflows, meaning that legal, compliance and brand reviews can run simultaneously and sequentially. For a major financial services brand that might otherwise route content through five sequential approval steps over five to seven business days, IntelligenceBank’s parallel workflow model can compress that timeline to a single business day — while generating a complete, time-stamped audit trail at every step. Importantly, when a risk is flagged and scored, the platform also provides guidance to the content author on how to fix the problem — not just that a problem exists.

Key capabilities in the review and approval phase

- Automated risk scoring: Every submitted file receives an AI-generated risk score, directing reviewer attention to the highest-risk content first.

- Inline proofing and annotation: Reviewers mark up files directly in the platform, with comments linked to specific text, images or sections.

- Parallel approval routing: Multiple stakeholders review simultaneously, eliminating sequential bottlenecks and compressing timelines.

- Version control: Full version history ensures the correct file is always in review, with changes tracked from brief to final approval.

- Configurable approval stages: Workflows can be tailored to match the organization’s governance structure, including escalation rules for high-risk content.

- Complete audit trail: Every review action, comment, approval and rejection is time-stamped and stored, providing a defensible record of the compliance process presented in advanced business intelligence reports.

For Australian financial services firms operating under ASIC’s expectation of documented compliance processes, the audit trail generated by IntelligenceBank’s workflow platform is itself a significant compliance asset — providing evidence that a systematic, governed review process was followed for every piece of published marketing content.

How Does Continuous Post-Publication Monitoring Protect Against Ongoing Risk?

The third and often most underestimated phase of marketing compliance operations is what happens after content goes live. For most financial services organizations, the compliance process effectively stops at the point of publication approval — but the regulatory risk does not. Interest rates change, product features are modified, promotional offers expire and regulatory guidance is updated, meaning content that was fully compliant on the day it was approved may present risk weeks or months later.

IntelligenceBank’s post-publication monitoring capability uses AI to continuously scan live digital channels — including the organization’s own websites, Google Ads, social media channels and the websites of distribution partners such as mortgage brokers, financial advisers, insurance aggregators and white-label product partners — flagging content that presents compliance, brand or regulatory risk. Alerts are generated automatically, without requiring manual auditor time for each site or page.

Why partner network monitoring matters

The practical implications for a financial services organization with a broker or adviser network are particularly significant. A major bank may have hundreds of accredited broker partners, each operating their own website and marketing materials. Ensuring that all of those partner sites accurately reflect current product terms, contain required disclosures and do not display expired offers is effectively impossible with manual audit processes alone. IntelligenceBank’s continuous monitoring scales to cover the full partner network, generating alerts and compliance reports without adding compliance headcount.

- Outdated rate and offer detection: Flags pages where comparison rates, promotional offers or product terms no longer reflect current information.

- Missing disclosure alerts: Identifies live pages where mandatory disclosure text has been removed or is absent.

- Partner site coverage: Scans the websites, landing pages and digital ads of distribution partners without requiring manual auditor time per site.

- Social channel monitoring: Continuously reviews social media content against the same regulatory and brand rules applied at the creation stage.

How Do All Three Phases Combine to Deliver Approval Efficiency?

The ten-times improvement in approvals efficiency that IntelligenceBank customers report is not the product of any single capability — it is the result of eliminating waste at every stage of the content lifecycle. Each phase addresses a distinct source of delay and risk: creation-stage checks prevent rework, workflow automation compresses review cycles, and post-publication monitoring closes the gap that opens after content goes live.

| Phase | What IntelligenceBank Does | Compliance Impact |

|---|---|---|

| 1. Content Creation | AI checks run inside Word, PowerPoint, Figma and Canva as the file is being authored. Risk flags appear inline before the file is saved. | Issues caught at source; zero rework cycles from late-stage compliance failures. |

| 2. Review & Approval | Automated risk score appears when file enters the workflow. Proofing tools allow annotated comments. Parallel approvals run simultaneously across legal, compliance and brand teams. | Review time cut from days to hours. Audit trail begins from first submission. |

| 3. Pre-Publication Check | Browser extension scans staged pages and PDFs submitted via email. Risks annotated in context, on the live page, before go-live. | Final gate prevents non-compliant content reaching customers or regulators. |

| 4. Post-Publication Monitoring | Continuous AI scanning of live websites, Google Ads, social channels and partner sites. Outdated rate offers, expired promotions and missing disclosures trigger immediate alerts. | Ongoing compliance as market conditions change; partner network covered without added headcount. |

When these phases operate together as a single integrated system — with content, compliance reviews, workflows, approvals, digital asset management (DAM) and post-publication monitoring all running on the same platform — content that previously took two weeks to move from brief to published can reliably be produced and approved in two to three days. Legal and compliance teams that previously spent the majority of their review time on routine low-risk checks can redirect that capacity to higher-value strategic work.

Advanced reporting and dashboard capabilities give compliance leaders and CMOs full visibility into the health of the content pipeline at any point — including volume of content in review, average approval cycle times, the most common risk types being flagged and the compliance status of the live digital estate. This data shifts compliance from a reactive function into a managed, measurable operational discipline.

What Is the ROI of Marketing Compliance Automation?

The business case for investing in AI marketing compliance software becomes clear once the true cost of manual review is visible. IntelligenceBank has developed two purpose-built ROI calculators to help Australian financial services organizations quantify the value of automation: the Content Risk Scanning ROI Calculator and the Website Scanning ROI Calculator.

Content Risk Scanning ROI Calculator

This tool estimates the time and cost savings from automating compliance reviews of marketing documents, PDFs, images and collateral. By entering the number of documents reviewed per month and average reviewer time, organizations can model the savings from reducing review time from hours to minutes per asset. IntelligenceBank customers have reported compliance reviews being completed in as little as two minutes per document.

Website Scanning ROI Calculator

This tool models the cost of continuously monitoring live web pages, Google Ads and partner sites for compliance risks, compared to the cost of periodic manual audits. For a major Australian bank or insurer operating dozens of product pages, hundreds of landing pages and a network of broker or adviser partner sites, the savings from automated monitoring compound significantly over time. Access both calculators at intelligencebank.com/resources/marketing-compliance-software-roi-calculator/.

| Metric | Manual Process (Typical) | With IntelligenceBank |

|---|---|---|

| Time per document review | Hours | As little as 2 minutes |

| Approval cycle time | 5–7 business days | 1 business day |

| Partner site monitoring | Periodic manual audit; coverage gaps | Continuous, automated, full network |

| Audit trail | Partial; inconsistent documentation | Complete, time-stamped, defensible |

How Do You Get Started with AI Marketing Compliance Software?

Making the cost of your current approach visible is the most effective starting point. Most financial services teams that run the numbers find the business case straightforward. IntelligenceBank’s ROI calculators are designed to do exactly this — converting reviewer hours and headcount into a concrete dollar figure that can be presented to finance and executive stakeholders.

From there, IntelligenceBank’s implementation team works directly with your legal and compliance stakeholders to configure risk rules that reflect your specific obligations — whether that is ASIC’s RG 234 requirements for rate advertising, APRA’s best financial interests duty for superannuation communications, ACCC prohibitions on misleading environmental, social and governance (ESG) claims, or your own internal brand and disclosure standards. Pre-built rule libraries for Australian financial services mean organizations can move from a manual process to automated reviews quickly, with premium professional services available to tailor the AI rules against specific products.

Implementation phases

- Baseline assessment: Run the ROI calculators to quantify the cost of manual review and identify the highest-volume content types and channels for initial automation.

- Rule configuration: IntelligenceBank’s implementation team collaborates with your legal and compliance stakeholders to build a rule library reflecting your specific regulatory obligations and internal standards.

- Authoring tool integration: Deploy native plugins for Word, PowerPoint, Figma and Canva so that risk checks run at the point of creation from day one.

- Workflow activation: Configure approval workflows to match your organization’s governance structure, including parallel routing, escalation rules and audit trail requirements.

- Post-publication monitoring setup: Define the web estate, Google Ads, social channels and partner sites to be continuously monitored, and configure alert thresholds and reporting.

IntelligenceBank is already trusted by leading financial services organizations across Australia, the United States and the United Kingdom to catch compliance risk faster and more accurately than any manual review process — across documents, websites, ads, social media and partner networks, all on one platform.

AI Marketing Compliance Software FAQs

What is AI marketing compliance software?

AI marketing compliance software automatically reviews marketing content — documents, images, web pages, ads and social media — against regulatory, legal and brand rules, flagging risks before publication and monitoring content continuously after it goes live. It differs from general content management tools in that it encodes specific regulatory requirements as machine-readable rules, applies them at production speed across the full content lifecycle, and generates a defensible audit trail of every review action.

Which Australian regulations apply to financial services marketing?

The four primary frameworks are ASIC (misleading financial promotions and unlicensed advice), APRA (superannuation and prudential governance), the ACCC under the Australian Consumer Law (misleading or deceptive conduct), and ACMA (digital, email and broadcast advertising). Asset managers also face specific obligations under ASIC’s Design and Distribution Obligations (DDO) and Target Market Determination (TMD) regime, as well as greenwashing enforcement priorities. Custom rules and additional regulatory frameworks can also be incorporated into IntelligenceBank’s rule library.

How does IntelligenceBank check content for compliance risks?

IntelligenceBank uses a combination of deterministic risk rules for non-negotiable requirements such as mandatory disclosures and prohibited phrases, and AI agents for more nuanced, contextual risks. Checks run inside authoring tools like Word, PowerPoint, Figma and Canva, inside the review and approval workflow, and continuously across live digital channels post-publication. Each check produces an inline flag that tells the content author not just that an issue exists, but how to resolve it.

Can IntelligenceBank monitor partner and distributor websites?

Yes. IntelligenceBank’s continuous monitoring capability covers not just your own web estate but also the websites, landing pages and digital ads of distribution partners such as mortgage brokers, financial advisers, insurance aggregators and white-label product partners — at scale, without adding compliance headcount. This is particularly valuable for banks and insurers with large accredited broker or adviser networks.

What ROI can financial services organizations expect from compliance automation?

ROI varies by organization, but IntelligenceBank customers have reported compliance reviews reduced to as little as two minutes per document and approval cycle times compressed from five to seven business days to a single day. IntelligenceBank provides two purpose-built calculators — for content scanning and website monitoring — at intelligencebank.com/resources/marketing-compliance-software-roi-calculator/. These calculators are based on real results from IntelligenceBank customers across enterprise financial services marketing teams.